The following is an excerpt from Kaulkin Ginsberg’s latest bi-annual industry report, The Accounts Receivable Management Review: Opportunities Abound (2015). Kaulkin Ginsberg is the foremost M&A and strategic advisor to the accounts receivable management industry, and this article covers some of the underlying causes for the burst in M&A activity our team observed during 2014. If you would like to confidentially discuss your interests in this dynamic market, please contact us at hq@kaulkin.com.

What’s behind the surge in M&A activity in the U.S. ARM industry?

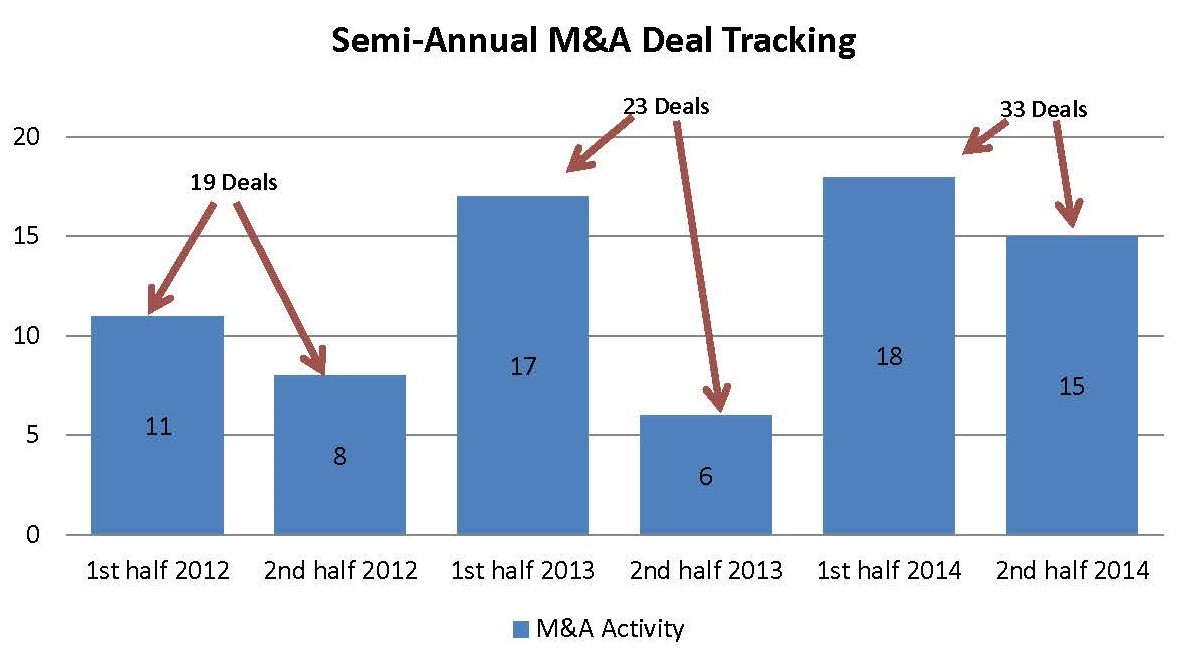

In 2014, the driving forces behind the increase in M&A activity were different from one market segment to another, but no segment was more active than mid-sized collection agencies. Seeking to offset market risk through diversification, many mid-sized agencies embraced mergers and acquisitions in an effort to increase service offerings, broaden their client base, and/or expand their geographic footprint. In 2014 alone, 10 transactions specifically involving mid-sized agencies were announced, the highest total since the start of the Great Recession.

Early in 2014, United Recovery Systems acquired Financial Health Strategies, a healthcare-focused ARM company. URS is well-known as a market leader within financial services, and this transaction provided the firm with diversification into healthcare services. URS also acquired Array Services last year, further positioning itself within the healthcare sector. Other companies who expanded during this time include Northland Group, who acquired Accounts Receivable Management to increase its client base and expand its service offerings, and Stoneleigh Recovery Associates, who purchased R&B Collections, positioning itself to strengthen its auto deficiency focus and R&B to strengthen its compliance program.

Beginning in 2013 on the debt-buying front, we experienced an uptick in sizeable M&A transactions, a trend that continued in 2014. Encore Capital Group, one of the largest U.S. debt buyers, got things started when it announced mid-2013 that it was buying a controlling interest in U.K.-based Cabot Credit Management. This marked the first time a U.S. debt buyer made a significant acquisition of another debt-buying company based in Europe. This came on the heels of Encore’s announcement it purchased Asset Acceptance earlier in 2013. At that time, Kaulkin Ginsberg forecasted that more U.S. debt buyers would acquire companies based outside the U.S. to fuel expansion efforts. However, we did not anticipate the magnitude of transactions that would follow. Portfolio Recovery Associates obtained Norway-based debt buyer Aktiv Kapital for $1.3 billion. Encore Capital Group announced it was buying U.K.-based debt buyer Marlin Financial Services for £295 million (approximately $481 million), and it finished acquiring the remainder of Cabot it did not purchase previously. Encore also bought Atlantic Credit & Finance (ACF), a leader in collecting fresh, higher-balance accounts, for approximately $70 million in cash. All told, nearly $2 billion changed hands in the debt-buying sector in less than two years.

In 2014, Kaulkin Ginsberg forecasted that a rapid consolidation would occur among debt buyers in the U.S. for the following reasons:

- Large credit card issuers dramatically reduced loan originations and delinquencies dropped as consumers paid off debt incurred prior to 2008, resulting in significantly less debt available for debt buyers to purchase directly. Kaulkin Ginsberg predicts more debt buyers will gobble up each other in an effort to feed their operations.

- The secondary debt-selling market had been completely decimated, impacting the profitability of debt buyers relying on resale to recuperate costs of buying large portfolios through secondary sales. The removal of the secondary debt-selling market also severely crippled the small (zip code) and mid-sized debt buyers, forcing them to look at other market segments for survival or selling their portfolios to larger debt buyers and shuttering operations.

- The significant and escalating cost of operating a debt-buying company created a true barrier to entry for new participants to form, resulting in fewer players overall.

- Overbearing compliance requirements made buying portfolios nearly impossible for most debt buyers who lack the stability and transparency demanded by the few issuers selling portfolios today. The few credit card issuers who were selling dramatically cut the number of debt buyers they sold to in order to comply.

- Emerging markets and other asset classes did not create a sustainable flow of new accounts to replace the shortfall from large issuers not issuing new credit at levels realized prior to the Great Recession.

We found that instead of selling out or merging operations, most debt buyers chose to stay the course and remain as a stand-alone business. We believe a consolidation among debt buyers will occur, albeit at a slower pace than we originally anticipated.

The largest divestiture in the U.S. ARM industry in 2014 was Expert Global Solutions’ (EGS) sale of its entire U.S. third-party collection operations, including its attorney network, education, healthcare bad debt, government and small business segments to private equity firm Platinum Equity, effectively removing the name NCO Group from the marketplace altogether. This transaction signified that private equity still looks favorably at collection agency transactions, a trend we expect to continue into the foreseeable future. To start 2015, West Corp. announced in January that it entered into a definitive agreement to sell its accounts receivable management and related agent businesses to Alorica, marking another large ARM company transaction to start the New Year.

Not to be outpaced, technology vendors in the ARM industry also made a number of significant moves in 2014, a trend we expect to continue in 2015. Leading software providers, identity management and fraud prevention solution providers, and loan brokers used mergers and acquisitions to position their companies to better service their credit grantor and collection agency customers.

On the collection law firm front, we started experiencing mergers in 2014 among some firms operating within the same state, such as the transaction that took place between law firms Fein, Such, Kahn & Shepard, P.C., and Levitan and Frieland, P.C., in New Jersey. While some expansion-minded collection law firms are seeking merger opportunities outside their states to enlarge their own footprint, this has been a slow and often fruitless process because very few players are unrealistic about the value of their operation or the deal terms needed to complete a transaction in this sector.

![[Image by creator from ]](/media/images/Finvi_Tech_Trends_Whitepaper.max-80x80.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)