In September 2014, Kaulkin Ginsberg wrote about Health Care and the Amazing Aging U.S. Population, a blog post discussing the implications of the baby boomer generation’s impending retirement.

Now, we take a look at some of the major regulations impacting both the U.S. health care system and the ARM industry, and how ARM providers can get involved with this expanding segment.

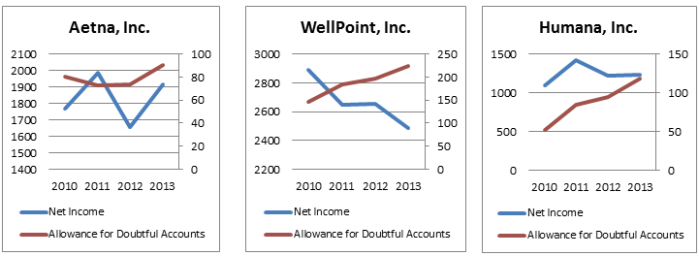

The Affordable Care Act – also known as “Obamacare” – created a new, growing market for uncollectible debt. As depicted in the graphs below, three of the largest health insurance providers participating in the Affordable Care Act are experiencing significant increases in their allowance for doubtful accounts. This is because many participants don’t fully understand their new insurance plans, especially when it comes to post-service billing procedures and high-deductible health savings accounts (HSAs). As a result, insurance providers have outsourced more of their work to stay on top of the influx of new clients.

Another regulation the ARM industry should consider is ICD-10, a massive overhaul of the medical coding procedures for health care providers. It will add nearly 68,000 new codes to the electronic health records (EHR) system. In the past, a hand injury may have been basically coded to read: “injured hand.”

Another regulation the ARM industry should consider is ICD-10, a massive overhaul of the medical coding procedures for health care providers. It will add nearly 68,000 new codes to the electronic health records (EHR) system. In the past, a hand injury may have been basically coded to read: “injured hand.”

Now, health care providers are required to submit a much more detailed description that would say: “left hand, vertical laceration from knife, 20 stitches used.” Failing to code properly could result in a rejected claim from federal or private insurance companies, costing the health care provider a lot of time and money. For these reasons, revenue cycle management (RCM) has become an integral component to health care provider operations.

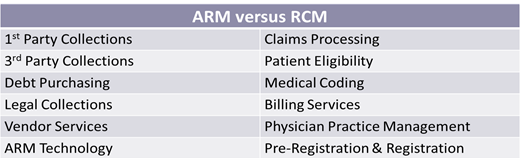

For those wishing to take advantage of the current excitement surrounding the health care segment, the list below serves as a basic guide for health care collection agencies considering a transition to RCM:

One of the best places for ARM providers to start is self-pay/co-pay services, which can complement their already ongoing third-party collection work. In most cases, they have existing technology infrastructure to handle this service. Additionally, the Affordable Care Act has increased the volume of self-pay/co-pay insurance claims, and that amount is expected to climb higher over the next few years. ARM providers would, however, need to work out the details of insurance knowledge and increased scrutiny by hospitals and other providers for “above and beyond” customer service, but this is not a foreseeable challenge.

One of the best places for ARM providers to start is self-pay/co-pay services, which can complement their already ongoing third-party collection work. In most cases, they have existing technology infrastructure to handle this service. Additionally, the Affordable Care Act has increased the volume of self-pay/co-pay insurance claims, and that amount is expected to climb higher over the next few years. ARM providers would, however, need to work out the details of insurance knowledge and increased scrutiny by hospitals and other providers for “above and beyond” customer service, but this is not a foreseeable challenge.

![[Image by creator from ]](/media/images/2015-04-cpf-report-training-key-component-of-s.max-80x80_F7Jisej.png)

![[Image by creator from ]](/media/images/Finvi_Tech_Trends_Whitepaper.max-80x80.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)