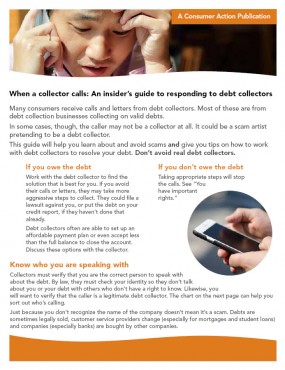

With millions of consumers receiving calls and letters from collectors every year—not all of them legitimate—Consumer Action has published “When a collector calls: An insider’s guide to responding to debt collectors.” Released today, as the Federal Trade Commission is holding the third of three public “Debt Collection Dialogues” in Atlanta, the free guide provides tips for communicating effectively with authentic collectors and avoiding impostors.

According to a CFPB report published in December 2014, nearly one-third of the 220 million consumers with a credit report have at least one account in collections. Scammers have used this to their advantage by making bogus collection calls and coercing consumers into either paying them or revealing bank account or other sensitive information. Consumers who don’t know their rights may find it difficult to tell the difference between a real collector and an impostor.

“When a collector calls: An insider’s guide to responding to debt collectors” gives consumers specific signs to look for—the use of profanity, a request for your full Social Security number or an unwillingness to provide specific information about the debt or who is calling, for example—that will help consumers determine whether a collection call is genuine or not. It also provides next steps, depending on that assessment. For collection calls and letters that are legitimate, the guide offers tips to help consumers deal with the debt proactively while preserving their rights.

Consumer Action created “When a collector calls” in partnership with the Consumer Relations Consortium (CRC), an association of leaders in the debt collection industry, making it a true “insider’s” guide.

“This is another case where the whole is greater than the sum of its parts,” said Linda Sherry, Consumer Action’s director of national priorities. “We often can achieve more by working together with seemingly strange bedfellows. Our collaboration with CRC has resulted in a publication that reflects the perspective of industry professionals, and that can be a benefit for consumers.”

“The CRC works to bring about positive industry reforms as it strives to ensure collectors pursue consumer debt obligations professionally. Incidents of immoral and unethical behavior by individuals purporting to be reputable professional debt collectors have tarnished the industry. It is our goal to have this guide help consumers identify illegal activity while encouraging their effective communication with trustworthy debt collectors,” said Pamela Baird, Esq., who serves as general counsel for New York-based Continental Service Group, Inc. (ConServe), an accounts receivable management services provider, and is a member of the CRC executive steering committee.

The English version of the three-page “When a collector calls” is available now for free download on the Consumer Action website. It soon will also be translated into Spanish. Related publications on debtors’ rights and the Fair Debt Collection Practices Act are also available.

About Consumer Action

Consumer Action has been a champion of underrepresented consumers nationwide since 1971. A non-profit 501(c)(3) organization, Consumer Action focuses on consumer education that empowers low- and moderate-income and limited-English-speaking consumers to financially prosper. It also advocates for consumers in the media and before lawmakers to advance consumer rights and promote industry-wide change.

By providing consumer education materials in multiple languages, a free national hotline, a comprehensive website (www.consumer-action.org) and annual surveys of financial and consumer services, Consumer Action helps consumers assert their rights in the marketplace and make financially savvy choices. Nearly 7,000 community and grassroots organizations benefit annually from its extensive outreach programs, training materials and support.

About the Consumer Relations Consortium

Consumer Relations Consortium (www.crconsortium.org) is a group of 20-plus leaders in the debt collection industry whose focus is on collecting the right debt, from the right consumer, in the right way. The group proactively engages with regulators and consumer advocacy groups to bridge the gap of understanding and expectations often present between consumers and collectors.

![the word regulation in a stylized dictionary [Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.png)

![Cover image for New Agent Onboarding Manuals resource [Image by creator from insideARM]](/media/images/New_Agent_Onboarding_Manuals.max-80x80_3iYA1XV.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)

![Whitepaper cover reads: Navigating Collections Licensing: How to Reduce Financial, Legal, and Regulatory Exposure w/ Cornerstone company logo [Image by creator from ]](/media/images/Navigating_Collections_Licensing_How_to_Reduce.max-80x80.png)