![[Image by creator from ]](/media/images/patrick-lunsford.2e16d0ba.fill-500x500.jpg)

[UPDATED Dec. 20, 10:11am to clarify that changes in debt collection law are central to the paper, and to add detail about the author’s position.]

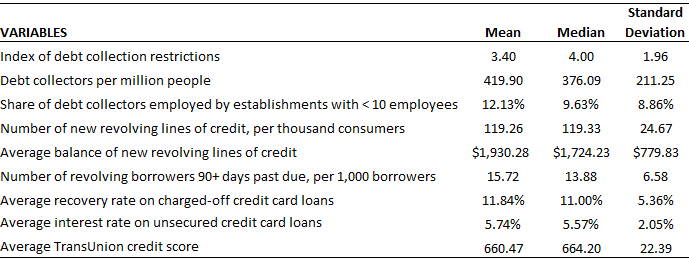

A working paper from the Federal Reserve Bank of Philadelphia argues that increased restrictions in the form of additional restrictions in state debt collection laws has a negative effect on both collection agency hiring in the state and on the extension of revolving lines of credit for consumers.

In a paper entitled “Debt Collection Agencies and the Supply of Consumer Credit,” author Viktar Fedaseyeu finds that for every new restriction codified in state law, the number of new revolving lines of credit decreased by 2.2 percent. The research found no such correlation with secured credit consistent with the notion that third party debt collectors are typically hired to help with unsecured credit.

The paper was published in May 2013 as a part of the Philadelphia Fed’s working paper series, and as such, do not necessarily represent the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System. Fedaseyeu is a visiting scholar of the Payment Cards Center at the Federal Reserve Bank of Philadelphia.

Fedaseyeu, an assistant professor of finance at the renowned Bocconi University in Italy, constructed a state-level index of the tightness of individual state debt collection laws, current through the end of 2012. Each state was assigned a score based on additional restrictions added to their collection laws; higher index scores indicated changes in law to a more restrictive environment for third-party debt collectors.

The research found that a more restrictive debt collection environment directly correlated to a lower number of debt collectors per capita. Fedaseyeu wrote that a one-point increase in the value of the state debt collection law index lowers debt collector density by 15.9 percent in that state.

Interestingly, the paper shows that most of the reduction in debt collection employment comes from larger debt collection agencies; the share of employment by small collection agencies (fewer than 10 employees) actually grows when debt collection laws are more stringent. A one-point increase in a state’s collection law index increases the share of collectors working at small firms by about 1.7 percentage points.

The effect of state laws on debt collector populations in a state had follow-on impact, according to the paper. Stricter regulations of debt collectors decrease recovery rates on charged-off unsecured credit cards by 1.1 percentage points for each additional restriction on debt collection activity. This, in turn, led to the reduction in new lines of revolving credit (-2.2 percent).

In his conclusion, Fedaseyeu notes, “In terms of policy implications, my results indicate that financial regulation that institutes strong consumer protection must be balanced with creditor rights in order for the latter to extend consumer credit in the first place.”

But Fedaseyeu also wrote that, “My results do not imply that credit expansion generated by more efficient debt collection is welfare improving, and further research is needed to shed light on this issue.” His research found that in states with a lower debt collection restrictions index score, the average interest rate on credit card accounts is higher and the average TransUnion credit score is lower.

Summary Statistics from the Study

For more on the study, listen to two ARM legal experts discuss the findings in a great 10-minute podcast.

![the word regulation in a stylized dictionary [Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.png)

![Cover image for New Agent Onboarding Manuals resource [Image by creator from insideARM]](/media/images/New_Agent_Onboarding_Manuals.max-80x80_3iYA1XV.png)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)

![Whitepaper cover reads: Navigating Collections Licensing: How to Reduce Financial, Legal, and Regulatory Exposure w/ Cornerstone company logo [Image by creator from ]](/media/images/Navigating_Collections_Licensing_How_to_Reduce.max-80x80.png)

![Whitepaper cover text reads: A New Kind of Collections Strategy: Empowering Lenders Amid a Shifting Economic Landscape [Image by creator from ]](/media/images/January_White_Paper_Cover_7-23.max-80x80.png)