![[Image by creator from ]](/media/images/patrick-lunsford.2e16d0ba.fill-500x500.jpg)

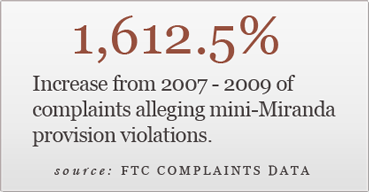

At the beginning of a collection call, a debt collector must recite a phrase that has become very familiar to the ARM industry, the “mini-Miranda” warning. It basically informs the consumer that the call is from a debt collector, that they are calling to collect a debt, and that any information revealed in the call will be used to collect that debt. The disclaimer must also be included in written correspondence with consumers, such as a collection letter.

It’s an important provision of the FDCPA. It prevents debt collectors from calling under false pretenses and gaining information from unwitting consumers that can later be used against them.

But did you know that complaints about failing to identify themselves as debt collectors has grown the quickest of all complaint types since 2007? In 2009, complaints about this behavior totaled 21,012, up from 1,227 in 2007…an increase of 1,612.5 percent!

Why the sharp increase? Well, we think it might have something to do with consumer attorneys and Web sites. Since the failure to include the warning in a letter is the single most verifiable FDCPA violation, consumers are told that this violation more than any other is a quick path to $1,000. And since lodging a formal complaint with the FTC is part of the litigious consumer playbook, complaints about mini-Miranda warnings have skyrocketed.

![the word regulation in a stylized dictionary [Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.png)

![[Image by creator from ]](/media/images/Thumbnail_Background_Packet.max-80x80_af3C2hg.png)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)

![Whitepaper cover reads: Navigating Collections Licensing: How to Reduce Financial, Legal, and Regulatory Exposure w/ Cornerstone company logo [Image by creator from ]](/media/images/Navigating_Collections_Licensing_How_to_Reduce.max-80x80.png)

![Whitepaper cover text reads: A New Kind of Collections Strategy: Empowering Lenders Amid a Shifting Economic Landscape [Image by creator from ]](/media/images/January_White_Paper_Cover_7-23.max-80x80.png)